Cost, Expense, Asset & Liability From Zero

- Ahtisham Asif Tantray

- Finance

- June 15, 2026

Table of Contents

Understand Cost, Expense, Asset, and Liability from first principles through the concept of transactions. Learn how economic sacrifice creates value and why these seemingly separate accounting concepts are actually connected parts of the same underlying framework.

Introduction

If you’ve ever studied accounting or finance, you’ve probably come across terms like Cost, Expense, Asset, and Liability. Unfortunately, these concepts are often taught as separate definitions that students are expected to memorize. One chapter explains Cost, another explains Assets, another explains Liabilities, and somewhere else Expenses are discussed. As a result, people may remember the definitions for an examination, but they rarely understand how these concepts are actually connected.

The truth is that these concepts are not independent ideas. They are deeply related to one another. In fact, all four emerge from a single underlying process. Once that process becomes clear, you no longer need to memorize definitions because the logic behind each term becomes obvious. Instead of treating Cost, Expense, Asset, and Liability as four isolated concepts, we will understand them from First Principles and trace them back to the source from which they originate.

That source is a transaction.

The One Concept Behind Everything

Most beginners assume that Cost, Expense, Asset, and Liability are four different topics. However, if we strip away the accounting jargon and focus on the fundamentals, we discover that all four are connected through transactions. Every asset exists because a transaction happened. Every expense exists because a transaction happened. Every liability exists because a transaction happened. Even cost itself only becomes meaningful within the context of a transaction.

This observation is powerful because it shifts our attention away from memorizing definitions and toward understanding a mechanism. Once you understand how transactions work, the remaining concepts begin to emerge naturally. Instead of learning four separate definitions, you learn one process and allow the definitions to reveal themselves.

What is a Transaction?

At its core, a transaction is simply an exchange of value between two parties. These parties are usually a buyer and a seller. Whenever something valuable is exchanged between them, a transaction takes place.

Consider a simple example. Imagine that you want to purchase a laptop. You approach a seller who owns the laptop and is willing to sell it. You give the seller ₹10,000, and in return the seller gives you the laptop. The money moves in one direction while the laptop moves in the opposite direction. Both parties give up something and both parties receive something.

What makes this exchange interesting is not the laptop itself but the structure hidden beneath it. You valued the laptop more than the ₹10,000, while the seller valued the ₹10,000 more than the laptop. Because both parties believed they would be better off after the exchange, the transaction became possible.

This seemingly simple event contains the foundation of Cost, Expense, Asset, and Liability.

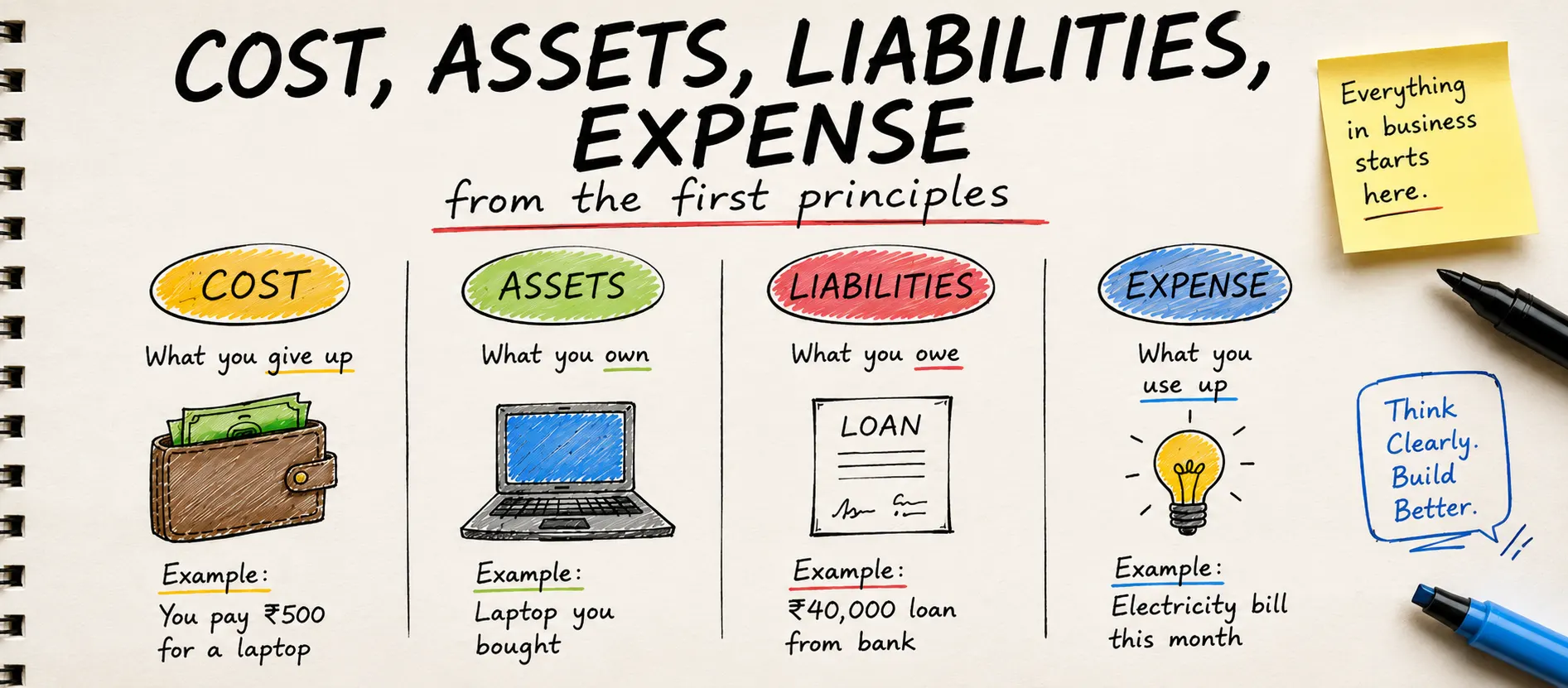

Understanding Cost

Most people automatically associate cost with money. While money is often involved, this interpretation is incomplete. Cost is much broader than simply spending cash. From a first-principles perspective, cost is an economic sacrifice made to acquire or produce something of value.

Returning to our laptop example, you sacrificed ₹10,000 in order to obtain the laptop. For you, the ₹10,000 represented the cost. However, from the seller’s perspective, the situation looks completely different. The seller sacrificed the laptop in order to receive ₹10,000. For the seller, the laptop represented the cost.

This reveals an important insight: cost is relative. The same transaction can contain different costs depending on whose perspective we examine. What is a cost for one party may be value for another party. For the buyer, the laptop is the value and the money is the cost. For the seller, the money is the value and the laptop is the cost.

This is also where many people misunderstand the word economic. Economic does not simply mean money-related. Economic refers to something scarce, limited, and valuable. Money is scarce, which is why giving it up can be an economic sacrifice. Time is scarce. Resources are scarce. Skills are scarce. Commitments are scarce. Whenever we sacrifice something scarce in order to obtain something valuable, we incur a cost.

If the thing being sacrificed has no scarcity and no value, it cannot really be considered an economic sacrifice, and therefore it cannot be considered a cost.

Cost is the Input of Every Transaction

A useful way to think about cost is to view it as the fuel of a transaction. Every transaction is a process, and every process requires an input. Cost acts as that input.

Without cost, transactions would not occur. If neither party is willing to give up anything, there is nothing to exchange and therefore no transaction can take place. Every transaction requires sacrifice from both sides, although that sacrifice may take different forms.

Once a transaction occurs, value changes hands. The interesting question then becomes: what happens to the value that is received?

The answer gives rise to three possible outcomes.

The Three Outcomes of a Transaction

When a transaction is completed and value is received, that value generally leads to one of three outcomes. It can become an Expense, an Asset, or a Liability.

The distinction between these outcomes depends entirely on what happens to the value after the transaction. Does the value disappear? Does it remain useful in the future? Or does the transaction create an obligation that must be fulfilled later?

The answers to these questions determine whether we classify something as an Expense, an Asset, or a Liability.

What is an Expense?

An expense arises when the value received from a transaction is consumed and no future economic benefit remains.

Imagine that you rent a room for thirty days. You stay in that room for the entire month and at the end of the month you pay the landlord ₹30,000. What exactly did you receive in return for your payment?

You received the ability to occupy and use the room for thirty days. However, by the time the payment is made, that benefit has already been consumed. The thirty days have passed. The value has been used up.

This is the essence of an expense. The value existed, but it did not survive into the future. It was consumed. Whenever a transaction provides value that is immediately used up and leaves no future economic benefit behind, we classify it as an expense.

An expense is therefore not merely money leaving your pocket. An expense is consumed value.

What is an Asset?

An asset arises when the value received from a transaction continues to provide benefits after the transaction has been completed.

Let’s return to the laptop example. When you purchased the laptop, did its value disappear immediately? Of course not. The laptop continues to exist. You can use it tomorrow, next month, or even several years from now. You can learn programming on it, perform graphic design work, earn income through freelancing, or even sell it to someone else in the future.

In other words, the laptop continues to provide future economic benefits.

This is the defining characteristic of an asset. If the value received from a transaction survives into the future and remains useful, it becomes an asset. An asset is essentially retained value—value that has not been consumed and can continue generating benefits later.

Whenever future economic benefit remains after a transaction, we are dealing with an asset.

What is a Liability?

Liability is slightly different because it does not emerge from future benefit. Instead, it emerges from future obligation.

Imagine that you borrow ₹1,00,000 from another person. The lender gives you the money today, but you do not give anything back immediately. At first glance, it may seem as though you incurred no cost. However, that is not true.

Your cost exists in a different form.

The sacrifice is not money; the sacrifice is commitment.

By accepting the loan, you commit yourself to repaying the money in the future. Perhaps you even agree to repay ₹1,10,000 after a few months. The lender sacrifices money today, while you sacrifice future freedom by taking on an obligation.

This is why economic sacrifice does not necessarily mean monetary sacrifice. Commitments are scarce and valuable too. By entering into the agreement, you have created a future obligation that must eventually be fulfilled.

That future obligation is called a liability.

Unlike an asset, which represents future economic benefit, a liability represents future economic sacrifice. It is value that will flow out of you in the future rather than value that will flow into you. In this sense, liability can be thought of as negative future value.

Whenever a transaction leaves us owing something to another party, we have created a liability.

The Pattern Hidden Behind All Four Concepts

At this point, a pattern begins to emerge.

Everything starts with a transaction. Every transaction requires a cost because both sides must sacrifice something of value. Once that cost is incurred and the transaction takes place, value is received. What happens to that value determines the final outcome.

If the value is consumed and no future benefit remains, it becomes an Expense.

If the value survives the transaction and continues providing future economic benefit, it becomes an Asset.

If the transaction creates a future obligation that must be fulfilled, it becomes a Liability.

Notice how all three concepts emerge from the same foundation. Cost sits at the base, and Expense, Asset, and Liability are simply different outcomes depending on the future nature of the value involved.

Conclusion

Most people try to memorize separate definitions for Cost, Expense, Asset, and Liability. The problem with this approach is that definitions are easy to forget. Understanding, however, is much harder to lose.

When viewed from First Principles, all four concepts become part of a single framework. Transactions require cost. Cost acts as the input. The transaction then produces an outcome. If the value is consumed, we call it an Expense. If the value remains and provides future economic benefit, we call it an Asset. If the transaction creates a future obligation, we call it a Liability.

Once you understand this flow, the entire topic becomes dramatically simpler. Instead of memorizing four definitions, you only need to understand one process.

And once you understand the transaction, everything else follows naturally.

Ahtisham Asif Tantray signing off!